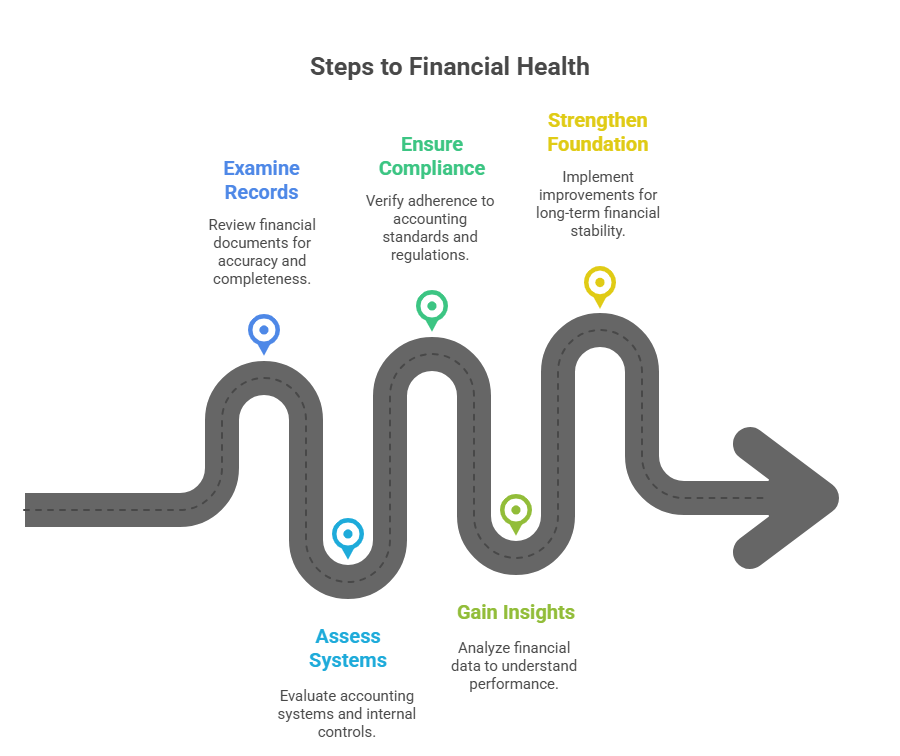

Running a small business successfully requires more than just passion and hard work — it also demands accurate financial management. Whether you are a startup founder, freelancer, or established small business owner, an accounting review plays a critical role in understanding your company’s financial health.

In simple terms, an accounting review is a detailed examination of your financial records, accounting systems, and internal controls to ensure that everything aligns with accounting standards and business goals. It’s not a full audit but provides valuable insights into your financial performance, compliance, and decision-making process.

In this comprehensive guide, we’ll explore what should be included in an accounting review for small businesses, why it matters, and how you can make the most of it to strengthen your financial foundation in 2025 and beyond.

1. What Is an Accounting Review?

An accounting review is an independent evaluation of a company’s financial statements and accounting practices conducted by a qualified accountant. Unlike an audit, which is more rigorous and involves verification of transactions and evidence, a review focuses on analytical procedures and inquiries to ensure financial statements are accurate and free from material misstatements.

For small businesses, this review helps verify:

- The accuracy of bookkeeping records

- Compliance with accounting standards and tax regulations

- Financial stability and cash flow trends

- Potential risks or discrepancies in financial management

It’s an essential tool for improving transparency, building investor confidence, and identifying financial inefficiencies.

2. Why Small Businesses Need Regular Accounting Reviews

Many small business owners believe that only large corporations need financial reviews. However, the opposite is true. In fact, smaller enterprises are more vulnerable to errors and cash flow problems because they often lack structured financial systems.

Here’s why regular accounting reviews are crucial:

a. Ensures Accuracy

An accounting review identifies data entry errors, missing receipts, or incorrect journal entries that can distort financial reports.

b. Strengthens Financial Decisions

Accurate financial data allows you to make informed business decisions, plan budgets, and allocate resources efficiently.

c. Improves Tax Compliance

A review ensures all transactions are properly recorded and categorized, making it easier to file accurate tax returns and avoid penalties.

d. Builds Investor and Lender Confidence

Lenders and investors are more likely to trust a business with reviewed financial statements that demonstrate credibility and transparency.

e. Detects Fraud or Mismanagement

By examining unusual transactions or inconsistencies, accounting reviews help prevent and detect financial fraud early.

3. Key Components of an Accounting Review

A thorough accounting review for small businesses should include multiple components that cover both financial statements and internal controls. Below are the most important areas to review.

3.1 Financial Statements Examination

The foundation of any accounting review lies in your financial statements, which reflect the overall financial health of your business. The main statements include:

- Income Statement (Profit & Loss Statement): Shows your revenue, expenses, and profit over a specific period.

- Balance Sheet: Displays your assets, liabilities, and equity to indicate financial stability.

- Cash Flow Statement: Reveals how cash moves in and out of the business, highlighting liquidity and cash management.

A professional accountant reviews these statements to ensure:

- Numbers are consistent across all documents.

- Transactions are properly classified (e.g., capital vs. operating expenses).

- Revenue recognition and expense reporting follow GAAP or IFRS standards.

3.2 Verification of Bank Reconciliations

Bank reconciliations are vital for verifying that your business bank accounts match your accounting records.

The review should confirm:

- All deposits and withdrawals are recorded correctly.

- Outstanding checks or deposits are properly tracked.

- Bank charges, interests, and foreign currency adjustments are included.

Frequent reconciliation helps prevent cash flow discrepancies and unauthorized transactions from slipping through unnoticed.

3.3 Review of Accounts Receivable and Payable

Effective management of receivables and payables is crucial for maintaining liquidity.

During the review:

- Accounts Receivable are checked to ensure invoices are issued on time and overdue accounts are followed up.

- Accounts Payable are examined for duplicate payments, early payment discounts, and vendor accuracy.

This helps improve cash flow forecasting and ensures your business maintains healthy relationships with clients and suppliers.

3.4 Payroll and Employee Expenses Review

Payroll errors can lead to financial losses and tax complications. Therefore, a detailed payroll review is a must.

Your accountant should check:

- Accuracy of employee salaries, bonuses, and benefits.

- Proper classification of employees vs. contractors.

- Correct calculation of tax withholdings, social security, and pension contributions.

- Compliance with local labor and tax laws.

For small businesses, payroll software integration can significantly reduce manual errors and simplify reporting.

3.5 Expense and Cost Review

One of the main objectives of an accounting review is to identify unnecessary or excessive spending.

During this step, your accountant will:

- Examine all operational and administrative expenses.

- Categorize expenses accurately (marketing, utilities, rent, etc.).

- Flag areas where cost optimization is possible.

This helps small businesses reduce overheads and increase profit margins without compromising quality.

3.6 Tax Compliance Check

Tax errors are one of the most common and costly mistakes small businesses face. The review ensures:

- Accurate calculation of corporate tax, VAT, and payroll taxes.

- Proper filing of returns before deadlines.

- Maintenance of tax records for audit purposes.

A professional accounting review minimizes the risk of penalties, audits, and compliance issues with tax authorities.

3.7 Internal Controls Evaluation

Internal controls are systems designed to prevent fraud and ensure accuracy in financial reporting.

A small business accounting review includes evaluating:

- Authorization processes for expenditures and payments.

- Segregation of duties to reduce fraud risk.

- Approval workflows for purchases and vendor payments.

- Data security for accounting software and financial records.

Strong internal controls are the backbone of financial transparency and accountability.

3.8 Inventory and Asset Management

If your small business holds inventory or fixed assets, these must be reviewed for accuracy and efficiency.

Your accountant should verify:

- Physical inventory matches accounting records.

- Valuation methods (FIFO, LIFO, weighted average) are consistent.

- Depreciation schedules for fixed assets are updated.

- Obsolete or slow-moving inventory is written down properly.

Effective inventory and asset management reduce losses, waste, and inaccurate reporting.

3.9 Review of Accounting Software and Systems

Many small businesses rely on accounting software like QuickBooks, Xero, or Zoho Books. A review should assess:

- Whether the software settings align with accounting best practices.

- Data accuracy and reconciliation features.

- Integration with payroll, CRM, and inventory systems.

- User access controls and security measures.

This ensures that technology is used effectively for real-time reporting and decision-making.

3.10 Financial Ratios and Performance Analysis

An accounting review isn’t just about accuracy — it’s also about insights.

Key financial ratios should be analyzed to measure performance and stability, such as:

- Gross Profit Margin

- Net Profit Margin

- Current Ratio

- Debt-to-Equity Ratio

- Return on Assets (ROA)

By comparing these ratios against industry benchmarks, small businesses can identify strengths, weaknesses, and opportunities for growth.

4. Frequency of Accounting Reviews for Small Businesses

How often should small businesses conduct accounting reviews? The answer depends on the business’s size, complexity, and transaction volume.

- Quarterly Reviews: Ideal for growing businesses or those with regular cash flow fluctuations.

- Bi-Annual Reviews: Suitable for established small businesses with stable financial operations.

- Annual Reviews: Minimum recommendation for all small businesses to ensure year-end accuracy before filing taxes.

Regular reviews keep your financial records current, accurate, and audit-ready at all times.

5. Benefits of Conducting Regular Accounting Reviews

A well-structured accounting review provides multiple benefits beyond compliance:

- Improved Decision-Making – Gain accurate insights into profitability and growth opportunities.

- Early Error Detection – Identify and fix discrepancies before they escalate.

- Enhanced Cash Flow Management – Optimize receivables and payables for better liquidity.

- Increased Credibility – Present transparent financial data to investors and lenders.

- Business Growth Support – Use data-driven insights to plan expansions or investments.

In short, an accounting review is an investment in your business’s long-term success.

6. Common Mistakes Small Businesses Make During Accounting Reviews

Even with the best intentions, small businesses often make avoidable errors during their accounting reviews. Here are the most frequent ones:

- Mixing personal and business expenses

- Failing to reconcile bank accounts regularly

- Ignoring minor accounting discrepancies

- Not updating accounting software or records

- Skipping professional consultation

Avoiding these mistakes can save time, money, and stress while improving your financial management practices.

7. When to Hire an Accounting Professional

While small business owners can perform basic financial reviews themselves, it’s often best to hire a certified accountant or accounting firm for a comprehensive analysis.

You should consider professional assistance if:

- You’re preparing for a bank loan or investor pitch.

- Your financial data has grown too complex.

- You’re facing tax audits or compliance issues.

- You’ve experienced consistent cash flow problems.

A professional accountant not only ensures compliance but also provides strategic insights to improve profitability and sustainability.

8. How to Prepare for an Accounting Review

Before starting an accounting review, small businesses should prepare by:

- Organizing financial documents (invoices, receipts, bank statements).

- Ensuring accounting software is updated with the latest transactions.

- Reconciling bank accounts and clearing outstanding items.

- Reviewing payroll and tax records for accuracy.

- Setting clear goals — e.g., identifying cost inefficiencies or improving cash flow.

Proper preparation helps ensure a smooth and efficient review process.

9. Tools and Technology to Simplify Accounting Reviews

In 2025, technology plays a significant role in making accounting reviews faster and more accurate. Tools that small businesses can use include:

- QuickBooks Online – For automated bookkeeping and expense tracking.

- Xero – For real-time financial reporting and multi-currency support.

- Zoho Books – For small business accounting and tax compliance.

- Wave Accounting – Free tool for freelancers and startups.

- Hubdoc or Dext – For receipt and document management.

Using these tools ensures accuracy, efficiency, and compliance while reducing manual work.

10. The Role of Accounting Reviews in Business Growth

An accounting review isn’t just about checking numbers — it’s about building a roadmap for success. By evaluating financial performance and improving systems, small businesses can:

- Identify profitable products or services.

- Manage expenses strategically.

- Forecast future cash flow accurately.

- Enhance creditworthiness and funding opportunities.

- Achieve long-term sustainability and scalability.

A well-executed review transforms financial data into actionable insights for smarter decision-making.

Conclusion

An accounting review for small businesses is not just a compliance requirement, it’s a strategic necessity. It ensures that your financial records are accurate, transparent, and optimized for better decision-making and growth.

By including key elements like financial statement analysis, internal controls, tax compliance, and expense review, you can build a strong financial foundation for your business.Remember, regular accounting reviews help you catch errors early, improve profitability, and stay compliant with changing tax laws. Whether you perform it quarterly or annually, make it a habit because in business, financial clarity is power.