In today’s dynamic business environment, corporate governance is not just about compliance—it’s about creating a culture of accountability, transparency, and ethical decision-making. At the heart of this governance structure lies the internal audit function, a critical mechanism that ensures organizations operate effectively, minimize risks, and protect stakeholder interests.

This comprehensive guide explores how internal audit strengthens corporate governance, highlighting its key roles, benefits, and best practices for modern organizations in 2025 and beyond.

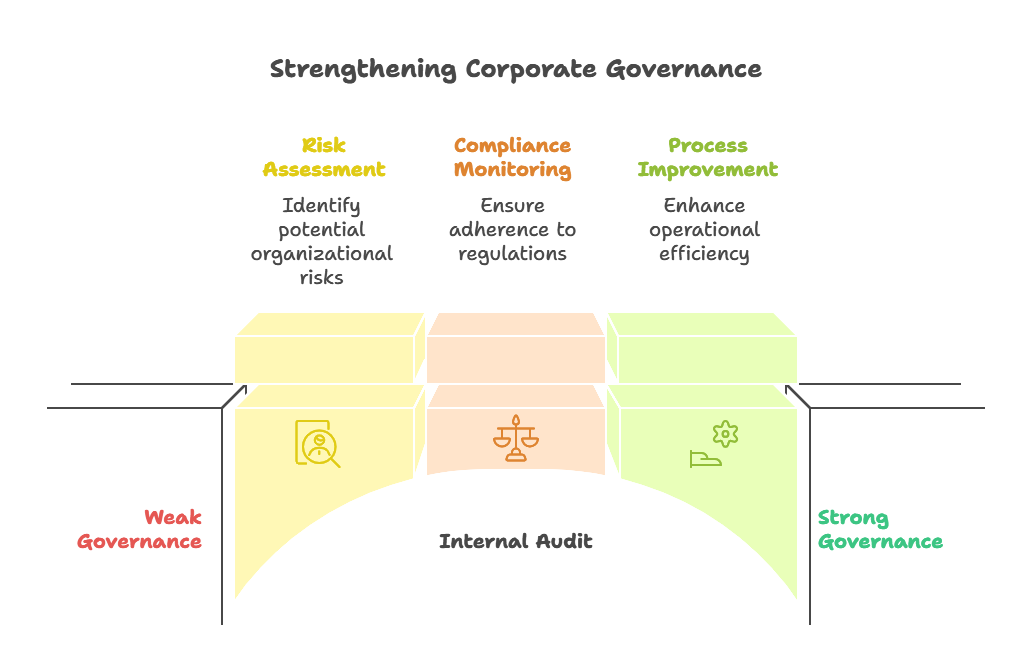

1. Understanding the Link Between Internal Audit and Corporate Governance

Corporate governance refers to the framework of rules, practices, and processes that direct and control a company. It ensures that business decisions align with the interests of stakeholders, including shareholders, employees, customers, and regulators.

Internal audit, on the other hand, is an independent and objective assurance function designed to evaluate and improve the effectiveness of an organization’s governance, risk management, and internal control processes.

In simple terms, internal audit acts as the watchdog of corporate governance—providing insights, assurance, and recommendations to strengthen operational efficiency and compliance.

2. The Role of Internal Audit in Corporate Governance

The internal audit department plays a pivotal role in enhancing governance by:

- Assessing internal controls to ensure that business processes operate efficiently and effectively.

- Evaluating risk management systems to identify vulnerabilities before they become major issues.

- Ensuring compliance with legal, regulatory, and corporate policies.

- Providing independent assurance to the board and audit committee about the integrity of financial reporting.

- Promoting ethical conduct and organizational accountability.

By maintaining objectivity and independence, the internal audit function serves as a bridge between management and the board of directors, providing an unbiased view of how well governance processes are working.

3. Strengthening Transparency and Accountability

Transparency is a cornerstone of good governance. Through regular audits and evaluations, internal auditors ensure that information disclosed to stakeholders is accurate, reliable, and timely.

Internal audits hold departments accountable for their actions by identifying process inefficiencies, policy violations, or misuse of resources. This fosters a culture of integrity and ensures decisions are made in the best interest of the company and its stakeholders.

4. Enhancing Risk Management Frameworks

In a rapidly changing business world, risks—financial, operational, cybersecurity, or reputational—are inevitable. The internal audit function helps organizations identify, assess, and mitigate risks before they escalate.

Through risk-based auditing, auditors focus their efforts on areas of highest risk. They evaluate how management handles these risks and whether the company’s risk appetite aligns with its strategic objectives.

By providing these insights, internal auditors not only protect the organization from potential threats but also enable strategic decision-making based on informed risk assessments.

5. Ensuring Compliance with Laws and Regulations

One of the most critical functions of internal auditing is ensuring regulatory compliance. As laws and industry standards evolve, businesses must stay compliant to avoid penalties and reputational damage.

Internal auditors conduct compliance audits to verify adherence to:

- Local and international laws

- Tax regulations

- Financial reporting standards

- Environmental and labor laws

- Anti-money laundering (AML) and anti-bribery policies

This proactive approach prevents legal issues and reinforces the organization’s reputation as a responsible and compliant entity.

6. Improving Financial Integrity and Reporting Accuracy

Sound corporate governance relies heavily on transparent and accurate financial reporting. Internal auditors review accounting processes, transaction records, and financial statements to ensure that data is free from errors, fraud, or manipulation.

They assess the internal control systems surrounding financial reporting to detect weaknesses or inconsistencies. When issues are found, auditors recommend improvements that enhance the credibility of financial information shared with investors, regulators, and the public.

Ultimately, internal audit ensures that financial decisions are based on trustworthy data, which boosts investor confidence and strengthens governance.

7. Promoting Ethical Conduct and Corporate Culture

Strong governance isn’t possible without a robust ethical culture. Internal auditors evaluate how well ethical standards are embedded across the organization.

They may conduct reviews of employee conduct, whistleblower mechanisms, and conflict-of-interest policies. By ensuring employees follow ethical guidelines, internal audit promotes responsible business practices that align with the company’s mission and values.

Moreover, internal audit can help detect and prevent fraud by monitoring red flags such as unusual transactions, policy violations, or deviations in operational behavior.

8. Supporting Strategic Decision-Making

Beyond compliance and risk control, modern internal audit teams play a strategic role in supporting leadership decisions.

By providing data-driven insights and objective evaluations, internal auditors help management make informed choices about resource allocation, new investments, or operational improvements.

Their recommendations often lead to greater efficiency, cost savings, and innovation, all of which contribute to stronger corporate governance and long-term success.

9. Strengthening the Role of the Board and Audit Committee

Internal audit serves as the eyes and ears of the board, especially through the audit committee.

The audit committee relies on internal auditors to provide independent assurance about the company’s risk posture, internal controls, and governance practices. This partnership ensures the board can make oversight decisions confidently and respond proactively to emerging issues.

When internal audit reports directly to the audit committee (rather than management), it reinforces independence and credibility—core principles of effective corporate governance.

10. Leveraging Technology for Stronger Governance

In 2025, digital transformation has reshaped internal auditing. Modern auditors use AI-powered tools, data analytics, and automation to conduct smarter, faster, and more comprehensive audits.

These technologies enable auditors to analyze large datasets, detect anomalies, and identify risks in real-time. This data-driven approach enhances accuracy and allows the internal audit function to provide predictive insights that strengthen corporate governance frameworks.

By leveraging technology, organizations can enhance transparency, reduce manual errors, and respond to governance challenges with agility.

11. Continuous Improvement Through Internal Audit Insights

A strong internal audit function does more than point out issues—it drives continuous improvement.

By regularly evaluating business processes and recommending enhancements, internal auditors foster a mindset of ongoing development and accountability. Their insights help organizations adapt to market changes, regulatory shifts, and internal challenges more effectively.

This cycle of assessment, feedback, and improvement forms the backbone of a resilient corporate governance structure.

12. Building Stakeholder Confidence

Ultimately, the effectiveness of corporate governance is measured by the trust of stakeholders—investors, employees, customers, and regulators.

Internal audit strengthens this trust by ensuring that the organization operates transparently, ethically, and in compliance with best practices.

When stakeholders know that a robust internal audit function is in place, they gain confidence in the company’s integrity and sustainability.

13. Best Practices for Effective Internal Audit Governance

To maximize the impact of internal auditing on corporate governance, businesses should adopt the following best practices:

- Ensure independence – Internal auditors should report directly to the audit committee or board.

- Adopt a risk-based approach – Prioritize audits based on areas of greatest potential impact.

- Leverage technology – Use data analytics for deeper insights and faster results.

- Encourage collaboration – Maintain open communication with management and board members.

- Focus on continuous learning – Keep auditors trained on new regulations, tools, and governance trends.

- Follow international standards – Adhere to frameworks like the Institute of Internal Auditors (IIA) standards.

These practices ensure that internal audit remains a powerful governance tool capable of adapting to future challenges.

14. Challenges in Aligning Internal Audit with Governance

Despite its importance, internal auditing faces challenges such as:

- Resource constraints

- Evolving regulatory requirements

- Resistance from management

- Complex global operations

Overcoming these requires strong leadership support, continuous process improvement, and a clear understanding of how internal audit contributes to organizational success.

Conclusion: Internal Audit as the Backbone of Good Governance

In summary, internal audit is not just a compliance function—it’s the foundation of effective corporate governance.

It strengthens transparency, fosters accountability, enhances risk management, and ensures ethical operations. With the integration of technology and strategic insight, internal audit empowers organizations to make informed decisions and build trust among stakeholders.As businesses evolve in 2025 and beyond, those that invest in a robust internal audit framework will not only meet governance standards but exceed them, setting the stage for sustainable growth and long-term success.